Future proofing

How worried should people be about their pensions? Mike Brewer and Parth Pandya break down the key takeaways from the Pensions Commission’s interim report.

For many, their pension is simply too boring, and too distant, to think about. But the Government should take credit for thinking about what living standards might look like in 2050, especially given we don’t even know who will be Prime Minister next month.

For those of you new to pension policy, it’s worth remembering that the first Commission 20 years ago was transformational. Its recommendations led to earnings uprating for the State Pension (later upgraded to the triple lock), a cut in the years of contributions required to qualify, as well as auto-enrolment. Fast forward two decades, and the second Commission’s interim report gives us a clearer view of how pension saving is going across the UK. It has concluded that, despite some commendable progress on pensioner incomes and poverty, too many are still on track for an inadequate income in retirement.

But how do we decide what counts as ‘on track’?

The first Commission used target replacement rates (TRR) (retirement income as a percentage of working-age earnings) to define ‘adequacy’. This approach puts a lot of weight on ensuring that people have roughly the same living standards in retirement as in working life. If you’re thinking this doesn’t sound like adequacy – which can be taken as putting a floor on pensioner living standards – you’d be right (a point we discussed in our own research). So last week’s report moved the thinking on by also considering what that floor should look like (measured in cold, hard cash), to set the bar for an acceptable standard of living in retirement.

The measure you use makes a massive difference. Tuesday’s headline was that 15 million, or four-in-ten, people are under saving before housing costs and before accounting for tax-free lump sum withdrawals. But that’s based on the TRR measure. Much more concerning was the Commission’s estimate that nearly 5 million people (13 per cent) are not even on track for a minimum retirement standard. This includes a disproportionate number of low earners, private renters, women, and the self-employed.

But defining an absolute level of adequacy is hard. The usual basket-of-goods approach – which costs material goods and social participation needed for a minimum standard of living – is subject to volatility, and is arguably skewed towards what higher earners spend rather than what lower earners need. The risk to such an approach is that it makes lower earners chase a floor that is a lot more than just ‘adequate’; a relative measure, on the other hand, keeps the floor connected to prevailing living standards. And it’s perfectly legitimate for governments to worry about whether people are setting themselves up for a big fall in their own standard of living when they retire (which is what is captured by a TRR), particularly given the complexity and uncertainties in both policy and investment decisions that individuals have to grapple with. And this may be why the Commission suggests that future policy should be guided by a hybrid measure that focuses on adequacy for low earners, but replacement rates for others.

How can we solve the problem of under-saving?

All measures agree that some people need to save more, but how can policy help? It’s possible that the Commission’s final report might consider: adjusting auto-enrolment based on labour market conditions and individual employment circumstances (e.g. bringing the self-employed into auto-enrolment); rethinking the Lower Earnings Limit (the point at which the government funnels people into pension saving) and whether the Upper Earnings Limit (the point at which you are left to fend for yourself) should remain tied to frozen Income Tax thresholds.

When thinking through these options, there are two points the Commission must consider. First, how to get more low and middle income families on track for a comfortable retirement without impoverishing them during their working lives. The second is whether it’s right to prioritise saving for retirement when the UK has low levels of financial resilience and precautionary savings: two-in-five working-age families have less than £1,000 in savings. On the latter, we think a ‘sidecar savings’ scheme – a tax-relieved, highly-liquid, savings account – which would siphon off some auto-enrolment funds with any extra balance rolling into a pension, would be a great first step.

The Commission also has thoughts on the Triple Lock, flagging that its formula creates long-run unpredictability about the level of the State Pension, making pension planning messy. What they didn’t mention is the important intergenerational issues at play. Since 2010, working-age benefits have grown at half the rate of the State Pension, and the Triple Lock has cost three-times more than initially expected (at £15.5 billion annually by the end of this Parliament). The Commission should work out what the State Pension should ultimately be worth, as a fraction of average earnings, and then recommend ending the Triple Lock at that level.

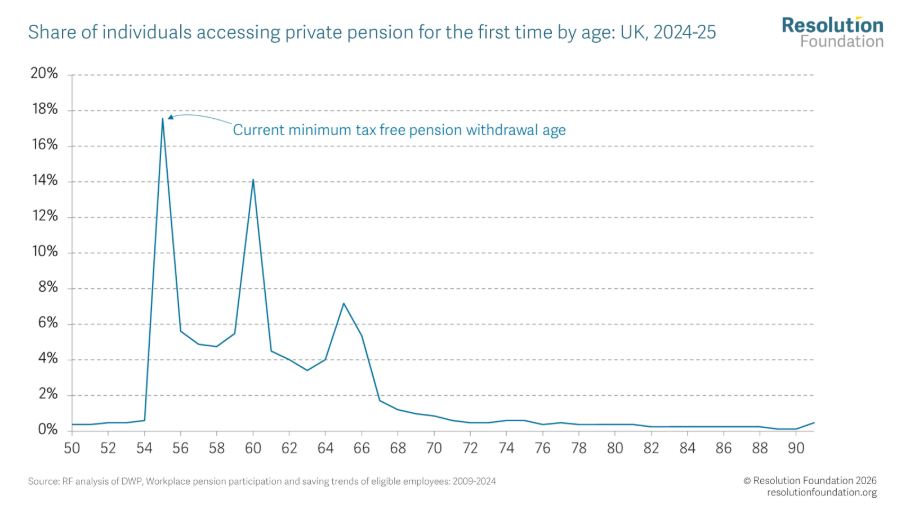

Pensions policy isn’t just about saving, but spending. As the chart below shows, in 2024-25 a staggering one-in-six people accessed their private pension at 55, the earliest possible date allowed and a full decade before the State Pension kicks in.

Early access encourages labour market exit or a reduction in hours. Given demographic changes are stretching retirement incomes, we should be incentivising people to work longer. Simultaneously encouraging retirement saving but allowing access to large sums of money pre-retirement is counterintuitive.

The Commission has a genuinely hard task of turning all of this into recommendations that are politically viable, fair to lower earners, and capable of delivering generational retirement security. The stakes couldn’t be higher: if they get it wrong, millions of people face a retirement defined by hardship rather than security.

| A guest post by

|